VAR Example Oil

by Professor Throckmorton

for Time Series Econometrics

W&M ECON 408

VAR¶

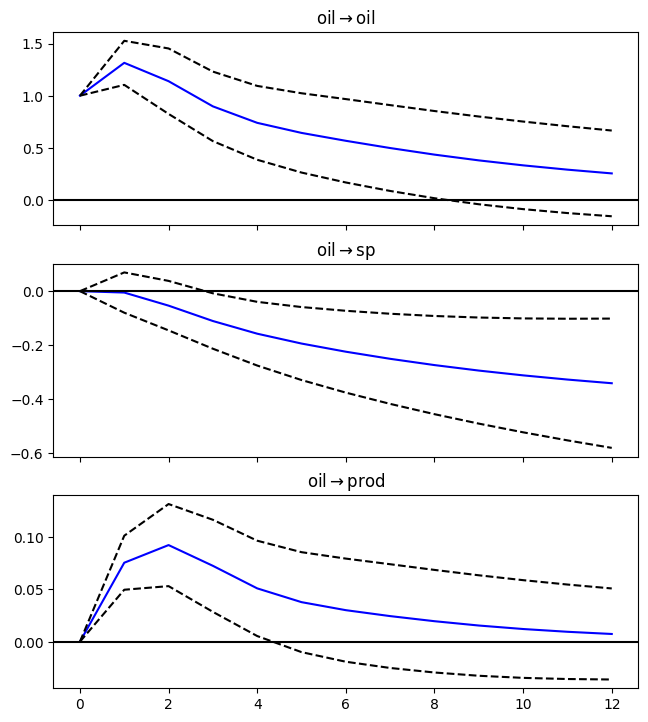

Big oil price increases are often associated with declines in production and asset prices. Read data on the price of crude oil (WTISPLC), industrial production (INDPRO), the S&P 500 (SP500), and the core consumer price index (CPILFESL).

# Libraries

from fredapi import Fred

import pandas as pd

# Setup access to FRED

fred_api_key = pd.read_csv('fred_api_key.txt', header=None).iloc[0,0]

fred = Fred(api_key=fred_api_key)

# Series to get

series = ['WTISPLC','INDPRO','SP500','CPILFESL']

rename = ['oil','prod','sp','price']

# Get and append data to list

dl = []

for idx, string in enumerate(series):

var = fred.get_series(string).to_frame(name=rename[idx])

dl.append(var)

print(var.head(2)); print(var.tail(2)) oil

1946-01-01 1.17

1946-02-01 1.17

oil

2026-01-01 60.04

2026-02-01 64.51

prod

1919-01-01 4.8739

1919-02-01 4.6585

prod

2026-01-01 102.3963

2026-02-01 102.5510

sp

2016-03-24 2035.94

2016-03-25 NaN

sp

2026-03-20 6506.48

2026-03-23 6581.00

price

1957-01-01 28.5

1957-02-01 28.6

price

2026-01-01 332.793

2026-02-01 333.512

# Concatenate data to create data frame (time-series table)

raw = pd.concat(dl, axis=1).sort_index()

# Resample/reindex to quarterly frequency

raw = raw.resample('ME').mean().dropna()

# Display dataframe

display(raw)/var/folders/dj/q2kc_rtn4kz50sd41yg6w8xc0000gq/T/ipykernel_36376/3185200006.py:2: Pandas4Warning: Sorting by default when concatenating all DatetimeIndex is deprecated. In the future, pandas will respect the default of `sort=False`. Specify `sort=True` or `sort=False` to silence this message. If you see this warnings when not directly calling concat, report a bug to pandas.

raw = pd.concat(dl, axis=1).sort_index()

Loading...

# Scientific computing

import numpy as np

data = pd.DataFrame()

# log real oil price

data['oil'] = 100*(np.log(raw['oil']/raw['price']))

# log real SP500

data['sp'] = 100*(np.log(raw['sp']/raw['price']))

# log industrial production

data['prod'] = 100*np.log(raw['prod'])

# Sample

#sample = data['03-01-2021':'02-28-2026']

sample = data

display(sample)Loading...

# VAR model

from statsmodels.tsa.api import VAR

# make the VAR model

model = VAR(sample)

# Search over candidate lag lengths

lag_selection = model.select_order(maxlags=12) # change 12 as needed

print(lag_selection.summary())

# BIC-selected lag

p = lag_selection.selected_orders['bic']

print("Selected lag by BIC:", p) VAR Order Selection (* highlights the minimums)

==================================================

AIC BIC FPE HQIC

--------------------------------------------------

0 14.26 14.34 1.564e+06 14.29

1 7.932 8.232 2785. 8.053

2 7.417* 7.942* 1665.* 7.630*

3 7.517 8.266 1842. 7.821

4 7.662 8.636 2133. 8.057

5 7.774 8.973 2395. 8.260

6 7.846 9.270 2586. 8.424

7 7.889 9.538 2717. 8.558

8 7.971 9.844 2973. 8.730

9 7.962 10.06 2979. 8.812

10 7.997 10.32 3128. 8.939

11 8.006 10.55 3212. 9.039

12 8.094 10.87 3579. 9.218

--------------------------------------------------

Selected lag by BIC: 2

/Users/vultureview/venv/myst-env/lib/python3.12/site-packages/statsmodels/tsa/base/tsa_model.py:473: ValueWarning: A date index has been provided, but it has no associated frequency information and so will be ignored when e.g. forecasting.

self._init_dates(dates, freq)

# Estimate VAR

results = model.fit(p)

# Assign impulse response functions (IRFs)

irf = results.irf(12)

# Plot IRFs

plt = irf.plot(orth=False,impulse='oil',figsize=(6.5,7.5));

plt.suptitle('');