VECM

by Professor Throckmorton

for Time Series Econometrics

W&M ECON 408

Slides

Summary¶

The Vector Error Correction Model (VECM) is specifically used for analyzing cointegrated time series that are first-order integrated, I(1).

VECM is builds on the concept of cointegration, i.e., each time series might be I(1), and certain linear combinations of them are stationary, I(0).

VECM is derived from a reduced-form VAR in levels when the data is cointegrated

VECM includes an error correction term that reflects the deviation from the lagged long-run average or “equilibrium”

VECM¶

Suppose is a VAR() with I(1), possibly cointegrated, variables in levels, then

is the first difference of a vector of non-stationary, I(1), variables, making them stationary. captures the short-run dynamics of the system, and is a vector of white noise errors.

is the cointegration structure, i.e., the long-run equilibrium relationship between variables in levels.

Cointegration Structure¶

If , there is no cointegration, and the model collapses to a VAR in differences.

If has reduced rank, , then , where:

is a matrix of cointegrating vectors.

is the error correction term, or long-run equilibrium errors.

is a matrix of adjustment coefficients, determining how fast each variable returns to the long-run equilibrium.

If is full rank, , then

there are independent stationary linear combinations,

and the whole vector must be stationary I(0).

The VECM is a restricted VAR in levels, where .

Rank of a matrix¶

A square matrix is full rank if its rank is . It’s not full rank, or has reduced rank, if its rank .

The following conditions are all equivalent — if any one is true, the matrix is full rank (warning: this is not a complete list)

Linearly independent columns: No column can be written as a linear combination of the others.

Linearly independent rows: No row is a linear combination of other rows.

Non-zero determinant: or

Invertibility: there exists such that

Examples¶

Example 1: Consider the following square matrix

Column 2 is column 1 is not full rank

Row 1 is row 2 is not full rank

# Scientific computing

import numpy as np

# Matrix

A = np.array([

[1, 2],

[2, 4]

])

# Rank

rank = np.linalg.matrix_rank(A)

print(f'rank(A) = {rank}')rank(A) = 1

det(A) = 0.0000

Example 2: Consider the following square matrix

We can’t multiply one row or column by a constant to get the other.

The determinant of a matrix is

Plug in the values

Since , the matrix is full rank.

# Matrix

A = np.array([

[3, 5],

[2, 4]

])

# Rank

rank = np.linalg.matrix_rank(A)

print(f'rank(A) = {rank}')

# Determinant

det = np.linalg.det(A)

print(f'det(A) = {det:.4f}')rank(A) = 2

det(A) = 2.0000

Example 3: For a square matrix

The determinant formula is .

That is a linear combination of the determinants of 3 () submatrices (i.e., a Laplace expansion).

See Determinant.

Example 4: Consider a VAR where all variables are stationary, , with

Then the VECM form is

with

This matrix clearly has full rank.

Cointegration¶

If some linear combination of non-stationary I(1) time series is stationary, then the variables are cointegrated, i.e., they share a stable long-run linear relationship despite short-run gaps (or errors).

Suppose we want to test for how many cointegrating relationships, , exist among , I(1), time series.

For example, if , then there are no cointegrating relationships, and if then all variables are cointegrated with eachother.

To justify estimating a VECM, there should be at least one cointegrating relationship between the variables, otherwise just estimate a VAR after first differencing.

Cointegration is about independent stationary linear combinations

You cannot have more independent stationary combinations than needed to eliminate all trends

Suppose there are , I(1), variables, then

| Rank, r = | Interpretation |

|---|---|

| 0 | no cointegration, 3 stochastic trends |

| 1 | 1 cointegrating relation, 2 trends |

| 2 | 2 relations, 1 trend |

| 3 | no trends → system is I(0) |

Johansen Cointegration Test¶

First, use the ADF (unit root) test to confirm that all time series are I(1).

The Johansen Cointegration Test has nested hypotheses

Suppose there are cointegrating relationships

Null Hypothesis: (i.e., the number of cointegrating relationships )

Alternative Hypothesis:

For each null hypothesis , if the test statistic critical value reject .

Then update until test fails to reject

In practice, use

coint_johansen()function fromstatsmodels.tsa.vector_ar.vecm.Choose lag length () for the VAR in differences.

Decide on deterministic components (constant/time trend) in the test.

Proceed to estimate a VECM if cointegration is found.

Example¶

The U.S. macroeconomy has gone through many important generational changes that might affect the cointegrating relationships between aggregate time series variables

E.g, The Great Depression, Post-War Period, Great Inflation of the late 1960s to early 1980s, The Great Moderation, The Great Recession (and the slow recovery), Post COVID

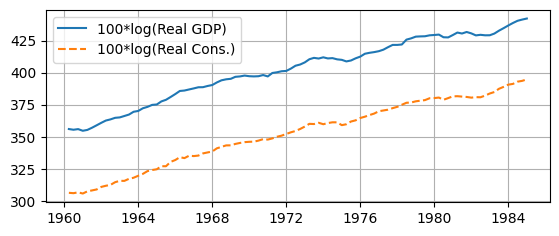

Let’s test whether consumption and income are cointegrated for the 25 years prior to the Great Moderation (1960-1984)

Measure them with log real PCE and log real GDP

Read Data¶

# Libraries

from fredapi import Fred

import pandas as pd

# Setup access to FRED

fred_api_key = pd.read_csv('fred_api_key.txt', header=None).iloc[0,0]

fred = Fred(api_key=fred_api_key)

# Series to get

series = ['GDP','PCE','GDPDEF']

rename = ['gdp','cons','price']

# Get and append data to list

dl = []

for idx, string in enumerate(series):

var = fred.get_series(string).to_frame(name=rename[idx])

dl.append(var)

print(var.head(2)); print(var.tail(2)) gdp

1946-01-01 NaN

1946-04-01 NaN

gdp

2025-07-01 31098.027

2025-10-01 31442.483

cons

1959-01-01 306.1

1959-02-01 309.6

cons

2025-12-01 21455.5

2026-01-01 21536.6

price

1947-01-01 11.141

1947-04-01 11.299

price

2025-07-01 129.430

2025-10-01 130.651

Create Dataframe¶

# Concatenate data to create data frame (time-series table)

raw = pd.concat(dl, axis=1, sort=False).sort_index()

# Resample/reindex to quarterly frequency

raw = raw.resample('QE').last()

# Display dataframe

display(raw.head(2))

display(raw.tail(2))Transform Data¶

data = pd.DataFrame()

# log real GDP

data['logGDP'] = 100*(np.log(raw['gdp']/raw['price']))

data['dlogGDP'] = data['logGDP'].diff(1)

# log real Consumption

data['logCons'] = 100*(np.log(raw['cons']/raw['price']))

data['dlogCons'] = data['logCons'].diff(1)

# Select sample

sample = data['01-01-1960':'12-31-1984']

display(sample.head(2))

display(sample.tail(2))Plot Sample¶

# Data in levels

sample_lev = sample[['logGDP','logCons']]

# Plot data

import matplotlib.pyplot as plt

fig, ax = plt.subplots(figsize=(6.5,2.5))

ax.plot(sample_lev['logGDP'],

label='100*log(Real GDP)', linestyle='-')

ax.plot(sample_lev['logCons'],

label='100*log(Real Cons.)', linestyle='--')

ax.grid(); ax.legend(loc='upper left');

ADF Unit Root Test¶

from statsmodels.tsa.stattools import adfuller

# Function to organize ADF test results

def adf_test(data,const_trend):

keys = ['Test Statistic','p-value','# of Lags','# of Obs']

values = adfuller(data,regression=const_trend)

test = pd.DataFrame.from_dict(dict(zip(keys,values[0:4])),

orient='index',columns=[data.name])

return testdl = []

for column in sample.columns:

test = adf_test(sample[column],const_trend='c')

dl.append(test)

results = pd.concat(dl, axis=1)

display(results)Note: the argument

const_trendsets whether the test accounts for a constant,'c'(default), and deterministic trend,'ct'.Fail to reject null for both time series in levels

Reject the null for both first-differenced time series

Since they are both , proceed to Johansen Cointegration Test

Trends¶

Stochastic trend, i.e.,

Can drift without bound — non-stationary

Deterministic trend, i.e.,

Deviations from the time trend are mean-reverting

Both deterministic and stochastic trends, i.e.,

First differencing will remove either/both trend(s).

# Control for deterministic time trend

dl = []

for column in sample_lev.columns:

test = adf_test(sample_lev[column],'ct')

dl.append(test)

results = pd.concat(dl, axis=1)

display(results)In

adfuller, settingregression = 'ct'allows for both a constant and linear time trend.Fail to reject the null that the data (after removing linear trend) has a unit root, i.e., removing the linear trend did not make the data stationary.

Conclusion: The data is consistent with a stochastic trend even after controlling for a deterministic trend.

Regardless, first differencing the data for the VECM will remove these trends, so we don’t need to account for them later.

Cointegration Test¶

# Johansen Cointegration Test

from statsmodels.tsa.vector_ar.vecm import coint_johansen

test = coint_johansen(sample_lev, det_order=1, k_ar_diff=1)

test_stats = test.lr1; crit_vals = test.cvt[:, 1]

# Print results

for r_0, (test_stat, crit_val) in enumerate(zip(test_stats, crit_vals)):

print(f'H_0: r <= {r_0}')

print(f' Test Stat. = {test_stat:.2f}, 5% Crit. Value = {crit_val:.2f}')

if test_stat > crit_val:

print(' => Reject null hypothesis.')

else:

print(' => Fail to reject null hypothesis.')H_0: r <= 0

Test Stat. = 25.85, 5% Crit. Value = 18.40

=> Reject null hypothesis.

H_0: r <= 1

Test Stat. = 3.69, 5% Crit. Value = 3.84

=> Fail to reject null hypothesis.

There is evidence that GDP and consumption are cointegrated.

det_order = 1includes a common constant and linear time trend from the cointegrating relationship.k_ar_diff = 1means we are using a VECM with 1 lag of differences.

Estimation¶

There is evidence that both GDP and consumption are I(1) and they are cointegrated.

If the data wasn’t cointegrated, they should be first differenced and estimate a VAR instead.

Proceed with estimating a bivariate VECM

where log real GDP and log real PCE and is their cointegrating relationship.

Model Selection¶

# Select number of lags in VECM

from statsmodels.tsa.vector_ar.vecm import select_order

lag_order_results = select_order(

sample_lev, maxlags=8, deterministic='co')

print(f'Selected lag order (AIC) = {lag_order_results.aic}')Selected lag order (AIC) = 1

In select_order:

deterministicsets which deterministic terms appear in the VECM, e.g.,deterministic = 'co'puts a constant outside the error correction to estimate the intercept since and have non-zero meansSelection criterion for lag order includes AIC and BIC (among others)

# Determine number of cointegrating relationships

from statsmodels.tsa.vector_ar.vecm import select_coint_rank

coint_rank_results = select_coint_rank(

sample_lev, method='trace', det_order=1, k_ar_diff=lag_order_results.aic)

print(f'Cointegration rank = {coint_rank_results.rank}')Cointegration rank = 1

In select_coint_rank:

method='trace'uses the Johansen Cointegration Testk_ar_diffis set to result of the AIC selection criterion.

Results¶

from statsmodels.tsa.vector_ar.vecm import VECM

# Estimate VECM

model_vecm = VECM(sample_lev, deterministic='co',

k_ar_diff=lag_order_results.aic,

coint_rank=coint_rank_results.rank)

results_vecm = model_vecm.fit()

tables = results_vecm.summary().tables

# Print summary tables

#for _, tab in enumerate(tables):

# print(tab.as_html())| coef | std err | z | P>|z| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| const | 16.8363 | 4.371 | 3.852 | 0.000 | 8.269 | 25.403 |

| L1.logGDP | 0.1289 | 0.100 | 1.290 | 0.197 | -0.067 | 0.325 |

| L1.logCons | 0.3300 | 0.123 | 2.677 | 0.007 | 0.088 | 0.572 |

| coef | std err | z | P>|z| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| const | 9.3086 | 4.419 | 2.106 | 0.035 | 0.647 | 17.970 |

| L1.logGDP | 0.1865 | 0.101 | 1.845 | 0.065 | -0.012 | 0.385 |

| L1.logCons | -0.1434 | 0.125 | -1.151 | 0.250 | -0.388 | 0.101 |

| coef | std err | z | P>|z| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| ec1 | -0.2361 | 0.063 | -3.764 | 0.000 | -0.359 | -0.113 |

| coef | std err | z | P>|z| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| ec1 | -0.1218 | 0.063 | -1.921 | 0.055 | -0.246 | 0.002 |

| coef | std err | z | P>|z| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| beta.1 | 1.0000 | 0 | 0 | 0.000 | 1.000 | 1.000 |

| beta.2 | -0.9444 | 0.015 | -64.031 | 0.000 | -0.973 | -0.916 |

Cointegrating Relationship¶

is the error correction term, i.e., the long-run equilibrium relationship between variables

If has reduced rank, , then , where is a matrix of cointegrating vectors.

Pi = results_vecm.alpha@results_vecm.beta.T

rankPi = np.linalg.matrix_rank(Pi)

print(f'alpha = {results_vecm.alpha}')

print(f'beta = {results_vecm.beta}')

print(f'Pi = {Pi}')

print(f'rank(Pi) = {rankPi}')alpha = [[-0.23609997]

[-0.12179596]]

beta = [[ 1. ]

[-0.9444435]]

Pi = [[-0.23609997 0.22298308]

[-0.12179596 0.1150294 ]]

rank(Pi) = 1

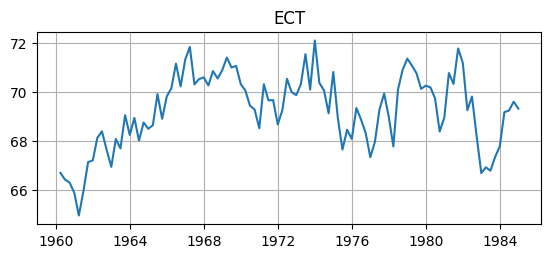

Error Correction Term¶

Interpreting the cointegration coefficients, or the error correction term (ECT)

The long-run linear relationship between GDP and consumption is strongly positive, , and the ECT measures how far away the system is from equilibrium.

(and is significant) measures how much GDP corrects disequilibrium, i.e., returns to equilibrium

The significance indicates which variables adjust, e.g., was not significant so consumption probably does not correct disquilibrium.

The sign indicates the direction of adjustment of each variable towards the long-run equilibrium, e.g., since , GDP pushes the system back to equilibrium

The magnitude is the speed or strength of adjustment, e.g., since , GDP adjusts more quickly than consumption.

# Error Correction Term

ECT = sample_lev@results_vecm.beta

ECT.name = 'ECT'

# Plot data

fig, ax = plt.subplots(figsize=(6.5,2.5))

ax.plot(ECT); ax.grid(); ax.set_title(ECT.name);

# Unit Root Test

test = adf_test(ECT,'c')

display(test)Result: reject that the ECT has a unit root and conclude that it is probably stationary, as desired.

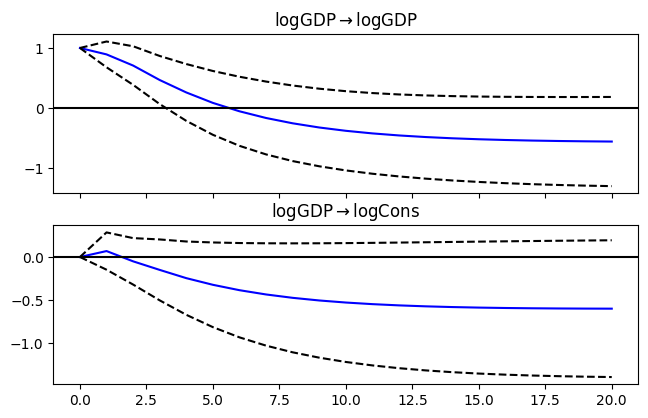

Impulse Response Functions¶

The estimated VECM cannot be used to compute IRFs

IRFs are only defined for a VAR with stationary time series or a VAR with cointegrated time series in levels (e.g., Christiano et al., 2005)

Instead we would estimate a reduced form VAR() separately to compute IRFs, where comes from the selected lag order from the VECM estimation

Then we can ask the question, how much does an increase in income change consumption and for how long?

Since both GDP and consumption are both clearly endogenous to many other things in the macroeconomy, it doesn’t make sense to use a Cholesky decomposition (e.g., orthogonalization) to estimate shocks.

# VAR model

from statsmodels.tsa.api import VAR

# make the VAR model

model_var = VAR(sample_lev)

# Estimate VAR(p)

results_var = model_var.fit(model_vecm.k_ar_diff + 1)

# Assign impulse response functions (IRFs)

irf = results_var.irf(20)# Plot IRFs

fig = irf.plot(orth=False,impulse='logGDP',figsize=(6.5,4));

fig.suptitle(" ");

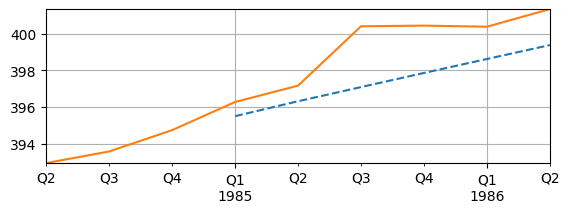

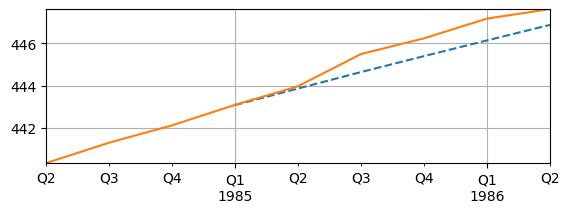

Forecasting¶

With the estimated VAR, forecasts can also be made

Want to compare forecasts to actual data

This may not be a great example because the 1980s is still relative volatile

# Lag order and end of sample

p = results_var.k_ar

last_obs = sample_lev.values[-p:]

# Forecast 6 quarters ahead

h = 6;

forecast = results_var.forecast(y=last_obs, steps=h)

forecast_df = pd.DataFrame(forecast, columns=sample_lev.columns)

dates = pd.date_range(start='03-31-1985', periods=h, freq='QE')

forecast_df.index = dates # Assign to index

# Actual Data

start_date = pd.Timestamp('12-31-1984')-pd.DateOffset(months=3*p)

end_date = pd.Timestamp('12-31-1984')+pd.DateOffset(months=3*h)

print(f'start date = {start_date}, end date = {end_date}')

sample_forecast = data[start_date:end_date]start date = 1984-06-30 00:00:00, end date = 1986-06-30 00:00:00

fig, ax = plt.subplots(figsize=(6.5,2))

forecast_df['logGDP'].plot(ax=ax, linestyle='--')

sample_forecast['logGDP'].plot(ax=ax, linestyle='-')

ax.grid(); ax.autoscale(tight=True);

fig, ax = plt.subplots(figsize=(6.5,2))

forecast_df['logCons'].plot(ax=ax, linestyle='--')

sample_forecast['logCons'].plot(ax=ax, linestyle='-')

ax.grid(); ax.autoscale(tight=True);